When is Your Organization Ready For Internal Controls?

The significance of internal controls cannot be overstated. These mechanisms are essential in safeguarding assets, ensuring accurate financial reporting, and maintaining compliance with laws and regulations.

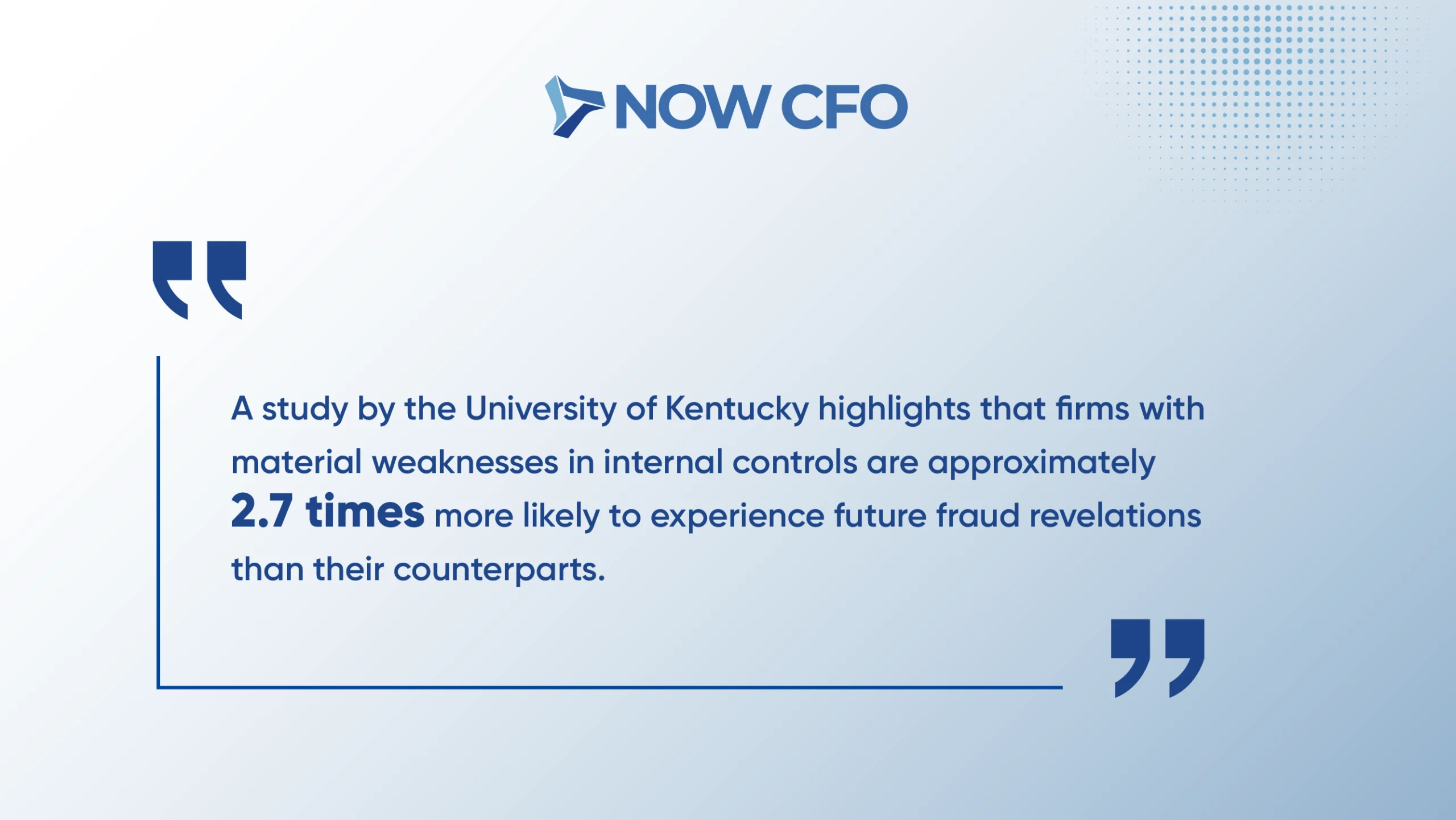

A study by the University of Kentucky highlights that firms with material weaknesses in internal controls are approximately 2.7 times more likely to experience future fraud revelations than their counterparts.

Understanding Internal Controls and Their Purpose

Establishing robust internal controls is a fundamental step for businesses aiming to maintain compliance with laws and regulations. These controls are the backbone of an organization’s risk management strategy, providing a structured approach to achieving operational efficiency and integrity.

Definition and Key Components of Internal Controls

Internal controls are systematic processes an organization implements to achieve its operational, reporting, and compliance objectives. These controls are not merely policies or procedures but are integrated into the organization’s daily activities, influencing behavior and decision-making at all levels.

The COSO outlines five interrelated components essential for an effective internal control system:

- Control Environment: Sets the organization’s tone, influencing its people’s control consciousness. It includes the integrity, ethical values, and competence of the organization’s people.

- Risk Assessment: Involves identifying and analyzing relevant risks to achieving objectives, forming a basis for determining how the risks should be managed.

- Control Activities: These actions are established through policies and procedures that help ensure management directives are carried out. They include approvals, authorizations, verifications, reconciliations, and segregation of duties.

- Information and Communication: Pertains to identifying, capturing, and exchanging information in a form and timeframe that enables people to carry out their responsibilities.

- Monitoring Activities: Processes that assess the quality of internal control performance over time, including regular management and supervisory activities, and separate evaluations.

Why Businesses Need Effective Internal Control Systems

Transitioning to the necessity of these systems, it’s evident that effective internal control systems in business are crucial for several reasons.

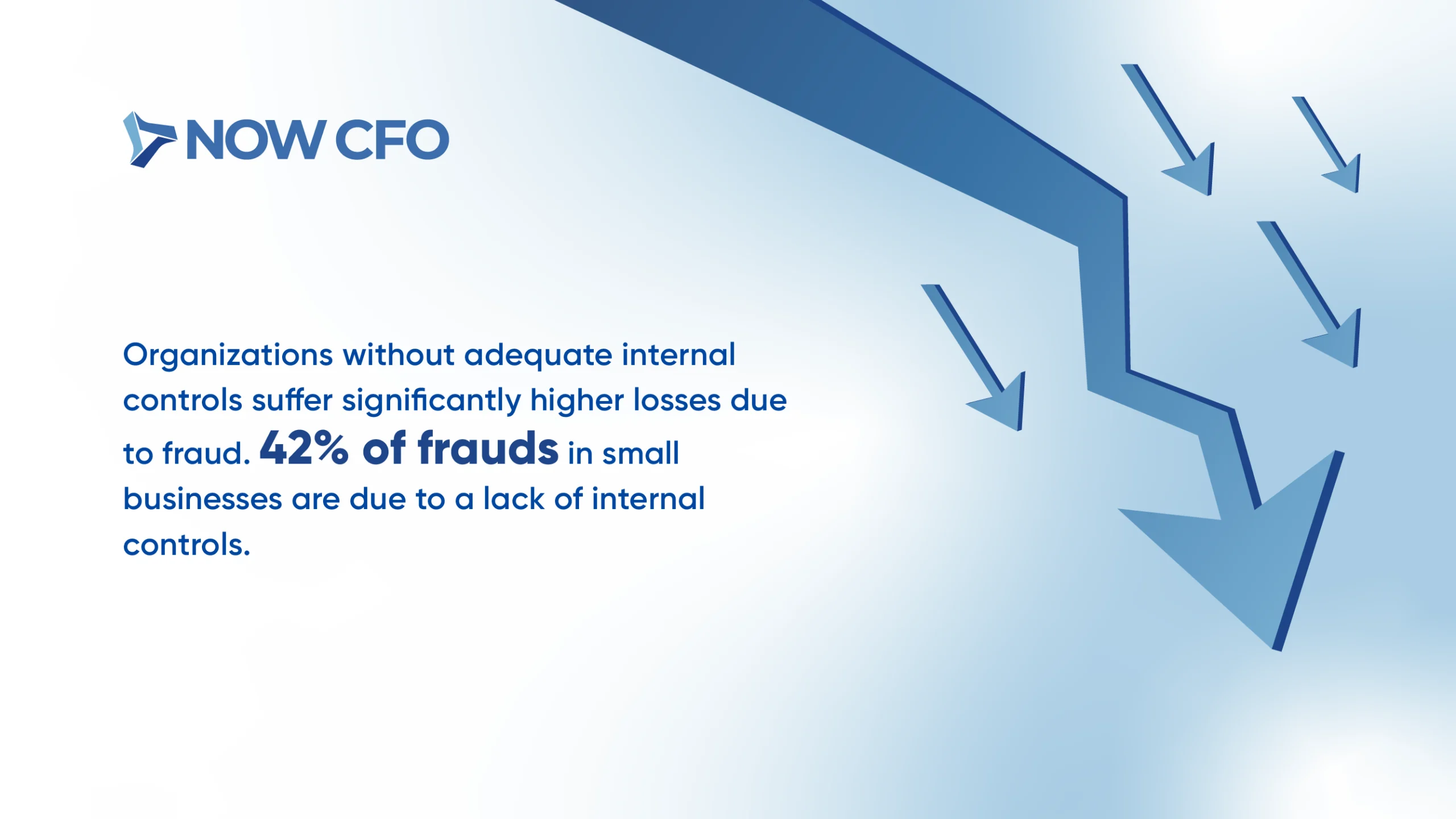

Firstly, they play an indispensable role in preventing fraud with internal controls. Organizations without adequate internal controls suffer significantly higher losses due to fraud. 42% of frauds in small businesses are due to a lack of internal controls.

Secondly, these systems enhance financial risk management by ensuring accurate and reliable financial reporting. This accuracy is vital for decision-making processes and maintaining investor confidence.

Moreover, compliance and internal controls go hand in hand. Regulatory frameworks like the SOX require stringent internal control measures to ensure transparency and accountability in financial reporting.

Additionally, effective internal controls contribute to operational efficiency by streamlining processes and reducing redundancies. They also protect assets from unauthorized use or disposition, ensuring the organization’s resources are used appropriately.

Common Misconceptions About Internal Controls

Despite their importance, several misconceptions about internal controls persist:

- Internal Controls are Only Necessary for Large Organizations

In reality, businesses of all sizes benefit from internal controls. Small businesses, in particular, are often more vulnerable to fraud due to limited resources and personnel.

- Implementing Internal Controls is too Costly

While an investment is necessary, the cost of not having internal controls, such as losses from fraud or regulatory penalties, can be significantly higher.

- Internal Controls are Only About Preventing Fraud

While fraud prevention is key, internal controls also ensure operational efficiency, accurate financial reporting, and compliance with laws and regulations.

- Once Established, Internal Controls Don’t Need to be Reviewed

Internal controls require regular monitoring and updating to remain effective, especially as the business environment and associated risks evolve.

- Internal Controls are the Sole Responsibility of the Accounting Department

Effective internal control is a collective responsibility, involving all levels of an organization, from top management to operational staff.

The Role of Internal Controls in Preventing Fraud

Establishing robust internal controls is vital for organizations aiming to maintain compliance. These controls serve as the first defense against fraudulent activities, providing a structured approach to risk management and operational efficiency.

How Internal Controls Detect and Prevent Fraudulent Activities

Effective internal controls are instrumental in detecting and preventing fraudulent activities within an organization. By implementing a comprehensive system of checks and balances, organizations can identify irregularities and deter potential fraudsters.

Key mechanisms through which internal controls mitigate fraud include:

- Segregation of Duties: Ensuring that no single individual controls all aspects of a financial transaction reduces the risk of unauthorized actions.

- Authorization and Approval Controls: Requiring managerial approval for significant transactions adds a layer of oversight.

- Reconciliations and Reviews: Regularly comparing internal records with external statements helps identify discrepancies promptly.

- Access Controls: Restricting access to financial systems and sensitive information minimizes opportunities for unauthorized activities.

Implementing Segregation of Duties to Reduce Fraud Risk

A critical component of internal control systems in business is the segregation of duties (SoD). This principle involves dividing individual responsibilities to reduce the risk of error or inappropriate actions.

For instance, in the procurement process, one employee might be responsible for ordering goods, another for receiving them, and a third for approving payments. This division ensures that no single individual controls all aspects of a transaction, making it more difficult to perpetrate and conceal fraudulent activities.

Implementing SoD requires careful planning and a clear understanding of organizational processes. It may involve:

- Identifying Key Processes: Determine which processes are most susceptible to fraud and require segregation.

- Assigning Roles Appropriately: Allocate responsibilities to divide critical tasks among multiple individuals.

- Regularly Reviewing Roles and Responsibilities: Ensure that changes in personnel or processes do not compromise the segregation of duties.

Identifying and Addressing Vulnerabilities in Financial Processes

Beyond implementing controls, organizations must proactively identify and address vulnerabilities within their financial processes. This involves thoroughly assessing existing procedures to detect weaknesses that could be exploited for fraud.

Common vulnerabilities include:

- Lack of Oversight: Insufficient supervision can lead to unchecked activities and increased risk of fraud.

- Inadequate Documentation: Poor record-keeping makes tracking transactions and identifying discrepancies difficult.

- Overreliance on Manual Processes: Manual procedures are more prone to errors and manipulation than automated systems.

To address these vulnerabilities, organizations should:

- Conduct Regular Audits: Periodic reviews help identify and rectify weaknesses in financial processes.

- Enhance Training Programs: Educating employees about fraud risks and prevention strategies fosters a culture of accountability.

- Leverage Technology: Implementing automated systems can improve accuracy and reduce the potential for fraudulent activities.

Ensuring Compliance Through Strong Internal Controls

Establishing robust internal controls helps maintain compliance with financial regulations and standards. These controls serve as a framework to ensure accurate financial reporting and adherence to laws, thereby safeguarding the organization’s integrity and reputation.

The Connection Between Internal Controls and Regulatory Compliance

Effective internal controls provide a systematic approach to managing risks and ensuring that financial reporting is accurate and reliable. By implementing these controls, organizations can detect and prevent errors or irregularities that could lead to non-compliance.

The SOX of 2002 underscores the importance of internal controls in regulatory compliance. SOX mandates that public companies establish and maintain an adequate internal control structure and procedures for financial reporting.

Section 404 requires management and external auditors to report on the effectiveness of these controls, emphasizing their role in ensuring compliance with financial reporting standards.

Furthermore, the COSO provides a widely accepted framework for designing and evaluating internal controls. The COSO framework outlines five interrelated components that collectively support compliance objectives.

Meeting Financial Reporting Requirements (GAAP, IFRS)

Regarding financial reporting, organizations must comply with GAAP and IFRS. These standards require accurate and transparent financial statements, achievable through effective internal control systems in business.

- GAAP Compliance: In the USA, GAAP provides the accounting standards for financial reporting. Implementing internal controls ensures that financial transactions are recorded accurately and consistently, facilitating compliance with GAAP requirements.

- IFRS Compliance: IFRS serves as the global standard for international financial reporting organizations. Robust internal controls help align financial reporting processes with IFRS, ensuring consistency and comparability across international boundaries.

Reducing Audit Risks with Well-Documented Internal Controls

Moreover, well-documented internal controls play an important role in reducing audit risks. Auditors assess the effectiveness of an organization’s internal controls to determine the extent of audit procedures required. Comprehensive documentation provides evidence of control implementation and operation, facilitating the audit process.

According to the COSO framework, continuous monitoring and evaluation of internal controls are essential for maintaining their effectiveness over time. This proactive approach allows organizations to promptly identify and address control deficiencies, thereby mitigating audit risks.

In addition, the SOX emphasizes the importance of internal control assessments in reducing audit risks. Section 404 requires management to produce an internal control report as part of each annual Exchange Act report, affirming the responsibility for establishing and maintaining adequate internal controls.

Improving Financial Accuracy and Risk Management

Maintaining precise financial records and proactively managing risks are paramount in today’s complex business environment. Robust internal controls are the backbone for achieving these objectives, ensuring that financial data is accurate and potential risks are identified and mitigated before they escalate.

How Internal Controls Enhance Financial Reporting Accuracy

Effective internal controls are instrumental in ensuring the accuracy of financial reporting. By implementing systematic procedures and checks, organizations can detect and correct errors promptly, thereby maintaining the integrity of their financial statements.

Key components that contribute to accurate financial reporting include:

- Segregation of Duties: Assigning different individuals to handle various aspects of financial transactions reduces the risk of errors and fraud.

- Reconciliations: Regularly comparing internal records with external statements helps identify discrepancies early.

- Authorization Controls: Ensuring that transactions are approved by appropriate personnel adds a layer of oversight.

According to the PCAOB, a material weakness in internal control over financial reporting may exist even when financial statements are not materially misstated. This underscores the importance of robust internal controls in maintaining financial accuracy.

Identifying and Mitigating Financial Risks Proactively

Proactive identification and mitigation of financial risks are crucial for organizational stability. Internal control systems in business play a pivotal role in this process by providing a structured risk assessment and management approach.

Key strategies include:

- Risk Assessment Procedures: Regularly evaluating potential financial risks allows organizations to implement controls that address these vulnerabilities.

- Monitoring Activities: Continuous oversight of financial processes helps in early detection of irregularities.

- Information and Communication: Ensuring that relevant financial information is communicated effectively across the organization supports informed decision-making.

The Impact of Poor Internal Controls on Business Stability

Moreover, inadequate internal controls can harm a business’s stability. Weak controls may lead to financial inaccuracies, increased vulnerability to fraud, and ultimately, loss of stakeholder confidence.

Consequences of poor internal controls include:

- Financial Losses: Errors and fraud resulting from weak controls can lead to significant financial setbacks.

- Regulatory Penalties: Non-compliance with financial reporting standards due to poor controls can result in fines and legal consequences.

- Reputational Damage: Stakeholders may lose trust in an organization that fails to maintain accurate financial records.

Key Elements of an Effective Internal Control System

This section delves into the foundational policies and procedures, the role of automation in enhancing efficiency, and the importance of ongoing monitoring and evaluation.

Policies and Procedures for Internal Control Implementation

Effective internal controls begin with well-defined policies and procedures that set the standard for organizational operations. These guidelines serve as a roadmap, ensuring consistency, accountability, and alignment with the organization’s objectives.

Key components include:

- Segregation of Duties: Dividing responsibilities among individuals to reduce the risk of error or inappropriate actions.

- Authorization Protocols: Establishing clear transaction approval hierarchies to prevent unauthorized activities.

- Documentation Standards: Maintaining comprehensive records to provide evidence of compliance and facilitate audits.

Automating Internal Controls for Efficiency

Incorporating automation into internal controls significantly enhances operational efficiency and accuracy. Automated systems minimize human error, streamline processes, and provide real-time monitoring capabilities.

Benefits of automation include:

- Real-Time Data Analysis: Immediate detection of anomalies or irregularities in financial transactions.

- Standardization of Processes: Ensuring consistent application of policies across the organization.

- Resource Optimization: Allowing personnel to focus on strategic tasks by reducing manual workload.

Automation tools can also facilitate compliance with regulatory requirements by maintaining detailed logs, providing audit trails, and supporting financial risk management efforts.

Monitoring and Evaluating Internal Control Effectiveness

Continuous monitoring and evaluation ensure that internal controls remain effective and adapt to evolving risks. Regular assessments help identify weaknesses, inform necessary adjustments, and reinforce the organization’s commitment to integrity and accountability.

Best practices for monitoring include:

- Periodic Reviews: Scheduled evaluations of control activities to assess performance and compliance.

- Feedback Mechanisms: Encouraging employee input to identify potential issues and areas for improvement.

- Use of KPIs: Tracking metrics that reflect the effectiveness of controls and inform decision-making.

Overcoming Common Internal Control Challenges

Organizations often encounter challenges that can impede the effectiveness of these controls. Addressing employee resistance, balancing control measures with operational flexibility, and strengthening controls in small and growing businesses are critical areas to consider.

Addressing Employee Resistance to Internal Control Policies

Employee resistance to internal control policies can stem from various factors, including fear of change, lack of understanding, or perceived additional workload. This resistance can undermine the effectiveness of control systems and expose the organization to risks.

To mitigate resistance:

- Engage Employees Early: Involve staff in developing and implementing internal control systems in business to foster ownership and acceptance.

- Provide Comprehensive Training: Educate employees on the importance of internal controls and how they contribute to the organization’s success.

- Communicate Benefits Clearly: Highlight how controls protect both the organization and its employees from potential fraud and errors.

Balancing Control Measures with Operational Flexibility

While stringent internal controls are vital for risk mitigation, overly rigid systems can hinder operational efficiency. Striking a balance between control and flexibility is crucial for optimal performance.

Strategies to achieve this balance include:

- Risk-Based Approach: Prioritize controls based on the level of risk associated with specific processes, allowing for flexibility in low-risk areas.

- Automated Solutions: Implement automation to streamline processes, reducing manual intervention while maintaining control integrity.

- Regular Reviews: Continuously assess and adjust controls to align with evolving business needs and operational dynamics.

Strengthening Internal Controls in Small and Growing Businesses

Due to limited resources and personnel, SMEs often face unique challenges in establishing effective internal controls. However, implementing tailored control measures is essential for sustainable growth and risk management.

Key recommendations:

- Segregation of Duties: Even with a small team, assign different individuals to handle various aspects of financial transactions to prevent errors and fraud.

- Leverage Technology: Utilize affordable accounting software to automate processes and maintain accurate records.

- Regular Audits: Conduct periodic internal audits to identify weaknesses and implement corrective actions promptly.

Conclusion: Taking Control of Your Business with Internal Controls

Implementing comprehensive internal controls is a strategic imperative for businesses aiming to fortify their financial health and operational resilience. By proactively addressing potential vulnerabilities and ensuring compliance, organizations can mitigate risks and enhance stakeholder confidence.

Take the first step towards fortifying your organization’s financial integrity and operational efficiency by partnering with NOW CFO. Contact our team of experts to develop a robust internal control strategy that propels your business towards sustained success.